On 21 March, Italian utility Enel S.p.A. (Enel) reported its preliminary 2023 full-year outcomes. The corporate confirmed a major lower within the share of thermal manufacturing to 27% in 2023 from 39% in 2022, ensuing from a greater than one-third decline in thermal output. Concurrently, the share of renewable vitality manufacturing (together with hydro) elevated to 61% in 2023 from 49% in 2022. These are prone to drive a major discount within the firm’s emission depth. However whether or not this is sufficient to meet its 2023 sustainability-linked bonds (SLBs) efficiency aim stays unsure.

Enel’s 2023 scope 1 emission depth intention of 148g of CO2 equal per kilowatt-hour (gCO2e/kWh) is tied to excellent SLBs of round €10 billion, representing a 35% discount from its 2022 degree of 229gCO2e/kWh. Enel would have needed to cut back its scope 1 emissions regarding energy technology by greater than 40% in 2023 to satisfy its goal (the corporate reported a decline of round 30% in whole emissions in 2023). Decrease coal output within the thermal combine may also help, however IEEFA estimates that it might take a mid-single-digit proportion discount in its common emission depth of thermal manufacturing to satisfy its goal.

1. Is Enel’s 2023 sustainability efficiency goal (SPT) formidable sufficient?

The reply might be sure. Enel’s 2023 scope 1 emission depth of energy manufacturing goal is predicated on its 2021-2023 Strategic Plan introduced in November 2020. It represents a 64% discount from its 2017 degree of 416gCO2e/kWh and units a path for an additional 45% decline to succeed in its 2030 goal of 82gCO2e/kWh.

IEEFA positively notes that the plan commits the corporate to a Science Based mostly Targets initiative-approved aim of an 80% greenhouse fuel emissions discount in 2030 versus 2017, consistent with a 1.5-degree pathway. The plan contains an intention of reaching 60 gigawatts (GW) of put in consolidated renewable capability (together with hydro) by 2023 versus 45GW in 2020, entailing an funding of €17 billion. It additionally commits the corporate to exit coal by 2027.

In 2022, Enel disposed of its Russian energy technology property together with primarily 5.6GW of typical capability, resulting in a discount in emission depth. Contemplating the 2023 emission depth goal stays because it was, it nonetheless seems sturdy, representing a 59% discount from its 2017 base of 365gCO2e/kWh (restated to exclude the impression of the disposal) and requiring a 51% discount to succeed in the restated 2030 intention of 72gCO2e/kWh.

2. What can be the monetary penalties of lacking the goal?

Extremely restricted. Enel has whole excellent SLBs of about €30 billion. All have a coupon step-up of 25 foundation factors (bps), which Enel must bear if it fails to satisfy the exams. About €10 billion of the bonds are topic to a check of 2023 targets, doubtlessly translating into further curiosity prices of roughly €25 million per 12 months. This represents merely 1% of its curiosity expense and 0.1% of its reported EBITDA in 2023. The quantity will lower with half of those bonds maturing in 2025 and 2026.

A step-up of 25 bps tends to be a typical market association. The monetary materiality relative to the corporate varies loads. Within the case of Enel, the step-up mechanism represents a really restricted monetary incentive, though the implications of a missed SPT will be broader from market and status views.

3. What would it not say about Enel’s transition plan?

IEEFA holds a basic view that lacking targets point out laggards in transition progress, which can increase climate-related credit score dangers. In consequence, the issuer’s bond spreads could widen because the dangers materialise, and the general price of capital could improve. SLBs—if appropriately priced—may act as an insurance coverage, with a step-up construction counteracting any rising dangers.

Anthropocene Mounted Revenue Institute first predicted in October 2023 that it was “extremely unlikely” that Enel would obtain its SPT, primarily based on interim operational information. It subsequently noticed that these bonds “have outperformed in comparison with each non-SLBs and SLBs whose targets have already been achieved”. The institute’s newest evaluation reveals that “the emissions depth goal remains to be a stretch […but] the likelihood of it being met has elevated”.

Whereas the variations in Enel’s emission depth in recent times will be considerably attributed to modifications in hydro and coal technology, its 2023 emissions discount is prone to be significant. If the corporate fails to satisfy the 2023 SPT, this doesn’t instantly conclude that Enel’s 2030 emission depth goal is out of attain. Nevertheless, Enel ought to proceed its actions to remain inside the 1.5-degree pathway and uphold the credibility of its broader transition plans.

In November 2023, Enel revealed a brand new 2024-2026 technique. Conspicuously, the corporate’s renewable vitality ambitions have been scaled again. It plans to speculate €12.1 billion in renewables between 2024 and 2026 and to succeed in a consolidated capability of 63GW by 2026—small progress from its earlier goal of 61GW by 2025. Enel has not explicitly up to date its 2030 renewables aim, however the firm’s “selective method” to renewables investments signifies that it’s going to fall quick. It will in flip require different means to attain its future emission depth discount targets.

Enel’s wind and photo voltaic vitality output elevated by about 10% in 2023, slower than in earlier years. The corporate could have to proceed to spice up the output of each via effectivity upgrades and restrain from fossil gasoline technology. Whereas the coal phaseout plan stays intact, the slower renewable buildout and an absence of different corrective actions could increase the chance of lacking future targets.

4. What classes ought to Enel be taught?

Enel continues to faucet the SLB market, issuing a complete of €1.75 billion in January 2024. IEEFA positively notes this dedication. The current SLBs have added 2026 to a strong checklist of check years that features 2024, 2025, 2030 and 2040, due to the corporate being a primary mover within the SLB market and its monitor report of sizeable choices.

Any indicators of not assembly the SPTs could have reputational implications. If Enel needs to sign continued seriousness to its transition plan, it ought to tighten its ambitions and keep away from the looks of setting easier-to-meet targets. As a substitute, Enel’s ambitions, in response to its newest sustainable financing framework set in January 2024, seem like much less sturdy than the earlier framework set in February 2023. The brand new 2026 scope 1 carbon depth goal of 125gCO2e/kWh reveals a mere 3.8% discount from its current 2025 intention. This leaves a better common annual discount of 13% between 2026 and 2030 to succeed in the 1.5-degree-aligned goal of 72gCO2e/kWh in 2030. The 2026 scope 1 and three carbon depth intention of 135gCO2e/kWh is flat from the 2025 ambition. Moreover, its put in renewable capability share targets have been lowered to 73% from 76% for 2025 and to 80% from 85% for 2030.

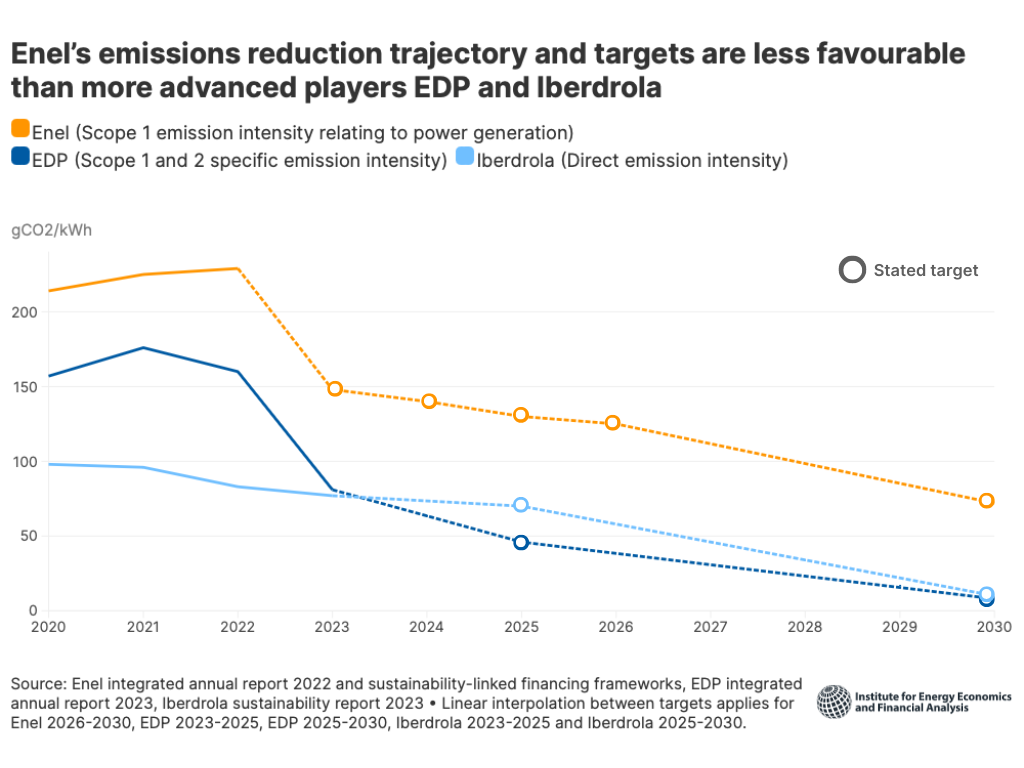

It’s price noting some extra superior gamers present extra beneficial trajectories in emission depth discount. For instance, Portuguese utility EDP decreased its 2023 scope 1 and a pair of emission depth by 50% 12 months on 12 months to 81gCO2e/kWh and has a goal of 8gCO2e/kWh by 2030. Spanish utility Iberdrola’s emission depth was 77gCO2e/kWh in 2023, with a goal of lower than 10gCO2e/kWh by 2030.

Apart from, Enel ought to ramp up its environmentally sustainable or European Union (EU) taxonomy-aligned investments. The goal of 80% alignment between 2024 and 2026 has seen no enchancment. A tighter ambition may convey Enel nearer to Iberdrola and EDP, which reported 89%-96% EU taxonomy-aligned capital expenditure (capex) in 2023.

5. Is the SLB market in hassle? Ought to issuers flip to make use of of proceeds inexperienced bonds as an alternative?

Enel issued €3.5 billion of inexperienced bonds between 2017 and 2019 however then grew to become the world’s largest SLB issuer. Its dedication to SLBs over inexperienced bonds is predicated on its desire to showcase its total technique, of which its tasks type an element.

Worries concerning the credibility of the SLB market have loomed lately. Based mostly on IEEFA’s calculations and Environmental Finance Knowledge, SLBs issuance in Europe decreased in two consecutive years from its peak in 2021, though the extent remains to be materially larger than in 2020 earlier than it skyrocketed. By comparability, inexperienced bond issuance in Europe reached a report excessive in 2023.

Use of proceeds inexperienced bonds are undoubtedly vital for investments within the net-zero transition. The upcoming European Inexperienced Bond Normal (EUGBS) may very well be groundbreaking. A current IEEFA report highlights its potential advantages for issuers via 4 pillars: commitments, capex pipelines, inexperienced asset supply and governance. Within the 2024-2026 technique, Enel maps out a complete gross funding plan of about €35.8 billion. Its 80% taxonomy-aligned capex goal (with proceeds primarily going to renewable technology and grids) signifies a sum of €28.4 billion being doubtlessly EUGBS-ready.

Having stated that, inexperienced bonds and SLBs serve completely different functions. SLBs exist as an revolutionary instrument that permits performance-based incentives to drive decarbonisation for all issuer varieties, from sovereigns to corporates. IEEFA believes the instrument stays helpful, significantly for hard-to-abate, high-emitting undertakings (“transition finance”). The Organisation for Financial Co-operation and Improvement outlines SLBs’ benefits to issuers over use of proceeds bonds: dedication enforcement, versatility, scalability and price discount potential.

A mixed construction can profit from each efficiency incentives and readability of use of proceeds, in IEEFA’s view. Austrian utility Verbund issued sustainability-linked inexperienced bonds in 2021. It reported yearly on its progress in the direction of attaining its efficiency targets and offered updates on tasks with allotted proceeds, which is sweet apply. Nevertheless, the instrument construction stays not often noticed out there.

Within the context of the EUGBS, one solution to construction a sustainability-linked inexperienced bond is to tie the efficiency targets to the instrument. For instance, targets will be primarily based on the anticipated bond proceeds’ contribution to environmental technique (e.g. taxonomy-aligned key efficiency indicators) and the impression of anticipated proceeds (e.g. annual electrical energy technology and averted emissions); such disclosure is already required at pre-issuance. This may increasingly act as an investor’s safety towards any underperformance or weak point within the closing contributions and impacts, finally creating extra depth to the sustainable bond market.

6. How can the SLB market’s credibility be improved?

The SLB market remains to be in a nascent stage. To enhance credibility, IEEFA believes that the overarching precept for an SLB construction is to allow significant decarbonisation progress. Therefore, the efficiency targets should be formidable sufficient: aligning to a 1.5-degree pathway throughout all scopes of emissions, explicitly avoiding carbon lock-in and selling enterprise transformation to “inexperienced” actions. Metrics to be measured towards must be complete, reflecting the “impression logic chain”. The probability of attaining them must be backed by a reputable transition plan.

Market members ought to take a extra nuanced and revolutionary method to allow wide-ranging types of monetary and/or structural options within the devices to cater to completely different nation, sectoral and particular person wants. Occasion triggers could transcend coupon step-up and embrace necessities of sure remedial actions, if relevant. The uniform 25 bps (or 50 bps) coupon step-up construction is straightforward to understand however doesn’t operate correctly.

Pricing premium at issuance must be measured rigorously to keep away from any misaligned incentives. The worth of the extra bond options ought to seize the anticipated acquire or loss ensuing from whether or not the targets are achieved or not.

The Worldwide Capital Market Affiliation Sustainability-Linked Bond Ideas have been established to help the transparency and credibility of SLBs. Optionally available disclosure for SLBs within the EUGBS regulation underlines the significance of transparency, however the SLB market stays unregulated. By late 2026, the European Fee is obliged to publish a report accompanied by a legislative proposal, the place applicable, on the necessity to regulate SLBs; IEEFA requires the European Fee to hurry up its legislative course of, given the approaching wants for a wider adoption of the instrument and its transitional, dynamic nature.

As market requirements and approaches take form, a sequence of SLBs which can be properly structured and properly complied with may characterize clear ambitions, robust readability of capex and motion plans, a excessive degree of confidence in plan supply and sturdy governance. Much like inexperienced bonds, this might in flip translate into decrease transition threat.